ORLANDO, Florida, May 22 (Reuters) – The curious dance between markets and the Federal Reserve now underway – Wall Street on a roll even as Fed officials say the most aggressive interest rate-hiking cycle in decades may need to go further – can partly be traced to the communications debacle of the “taper tantrum” exactly 10 years ago.

On May 22, 2013, then Fed Chair Ben Bernanke revealed for the first time that the central bank might soon begin scaling back its asset purchase program, triggering a wave of panic, volatility and uncertainty that crashed over world markets.

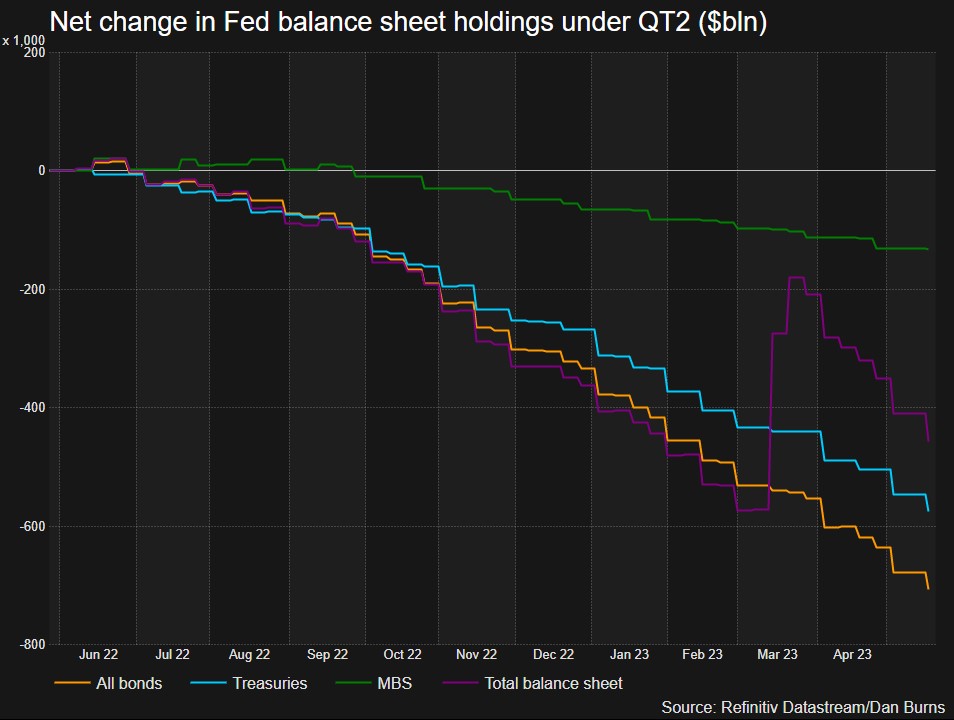

As much as asset prices got slammed, greater damage was done to the Fed’s credibility. Fear of a repeat influenced subsequent policy signaling, and ultimately helped shape the Fed’s eventual shift to twin rate hikes, ending so-called quantitative easing (QE) and starting quantitative tightening (QT).

The Fed was much more meticulous after 2013 in laying out its various moves to withdraw stimulus. Markets were far better prepared when the time came in 2022 for the Fed to simultaneously raise rates and reduce its balance sheet.

But as some argue, in its quest to avoid another taper tantrum, the Fed delayed that two-pronged tightening too long, which has partly contributed to the stickiness of inflation today.

Paul McCulley, adjunct professor at Georgetown University and former chief economist at bond giant Pimco, notes that the communications groundwork for rate hikes and QT began in September 2020. The first rate increase was in March 2022 and QT began three months later.

This lengthy buildup may have averted another taper tantrum, but tied the Fed’s hands on raising rates even as inflation was roaring back.

“The ‘cure’ for what happened a decade ago – the market jumping the gun on liftoff — itself became a problem this cycle: a forward guidance straight jacket that delayed the much-needed policy rate liftoff,” McCulley said.

COMMUNICATION BREAKDOWN

Answering a lawmaker’s question during an appearance before Congress’ Joint Economic Committee on May 22, 2013, Bernanke said: “If we see continued improvement and we have confidence that that’s going to be sustained then we could in the next few meetings … take a step down in our pace of purchases.”

Markets thought this not only meant the Fed would soon “taper” its bond purchases, but also raise interest rates. They went into a frenzy.

In a matter of weeks, the S&P 500 fell 8%, world stocks fell 10%, emerging market currencies and stocks fell 5% and 15%, respectively, and the 10-year Treasury yield shot up to 3% from 2%.

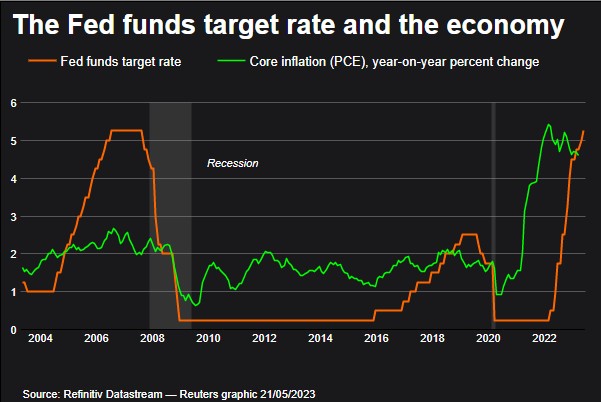

Emerging markets were hit especially hard, due to their exposure to dollar-denominated debt and U.S. borrowing costs. They have also been at the sharp end of the Fed’s current tightening campaign of 10 consecutive rate hikes worth 500 basis points and the launch of “quantitative tightening” or QT.

U.S. markets, however, have been less rattled. The S&P 500 is only 5% off where it was in March last year when the hikes started and is up nearly 10% this year. So far this year, the Nasdaq is up more than 20% and Treasury yields are lower.

Willem Buiter, a former policymaker at the Bank of England, said markets have taken the rate hikes and QT in their stride because the policy changes were well signaled. The Fed and markets have learned their lessons from the taper tantrum.

“Markets have learned about the conditions under which QT and multiple rates hikes will take place and proceeded. And the Fed has improved its communications relative to what we saw 10 years ago, which was a bit of an own goal,” Buiter said.

Bernanke and his peers can be cut a fair amount of slack. May 2013 was a fragile time – less than five years since the collapse of Lehman Brothers, and less than a year since then European Central Bank chief Mario Draghi saved the euro with his “whatever it takes” remarks.

Deflation, not inflation, was the fear.

As other central bankers discovered, getting out of the zero interest rate policy (ZIRP) and QE regime was a whole lot more complicated than getting into it.

Former Bank of England governor Mark Carney infamously said once UK unemployment fell below 7% interest rates would go up – it did, they didn’t – earning him the sobriquet “the unreliable boyfriend.”

Andrew Sentence, a former BoE rate-setter and one of the most consistently hawkish policymakers in recent times, says the taper tantrum was just one example of many miscommunications at the time from central banks trying to unwind stimulus.

“If you want to signal a change in policy it has to be planned and part of a consistent communications strategy form the central bank. Maybe the taper tantrum illustrates that it wasn’t as planned and consistent as it should have been,” he said.

(The opinions expressed here are those of the author, a columnist for Reuters.)

By Jamie McGeever

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.